This article is part of the series, Post-COVID-19: How Governments Should Respond to Fiscal Challenges to Spur Economic Recovery, coordinated by the International Tax and Investment Center (ITIC) to offer tax policy guidance to developing countries during the post-pandemic recovery phase.

In this installment, Oxford Economics analyzes the impact that the coronavirus pandemic will have on emerging markets and the wider world in 2020.

Copyright 2020 Oxford Economics and ITIC. All rights reserved.

The coronavirus and the policies adopted to fight it are set to have a massive negative impact on output in emerging markets and the wider world in 2020. A variety of factors including demographics, social conditions, health care systems and structural economic vulnerabilities will affect how badly emerging markets are hit, both as a group and individually, with Latin American economies perhaps most at risk. Large rises in budget deficits and public debt are also likely across most emerging markets. The rises in public debt we forecast do not look unmanageable in most cases, but market tolerance for fiscal slippage tends to be lower for emerging economies than for the advanced economies, and there may be a number of economies for which pressures on public finances will be sufficiently large to cause financial jitters this year. The authorities in emerging markets face a balancing act between trying to avoid fiscal efforts spilling over into financial instability and preventing real economic distress that can spill over into social and political unrest.

The Impact of Coronavirus and Containment Policies on the World Economy

The coronavirus is set to have a massive negative impact on world output in 2020. The combination of supply disruptions and demand destruction caused by the virus, and by the policies adopted to combat it, point to global GDP falling this year at the fastest pace since World War II. We forecast a drop of nearly 4 percent in world GDP during 2020, with the decline concentrated in the first half of the year during which we expect a slump of some 7 percent.

A key factor behind this collapse in activity is the economic impact of social distancing and lockdowns. Around 40 percent of consumer spending in sectors such as tourism, restaurants, hotels, and cinemas and also clothing and car purchases, normally occurs in crowded areas or social situations. A large chunk of this “discretionary” consumer spending will be postponed, and some of it will be lost permanently. With much of this spending being on services, the 2020 global recession will be unusually “services heavy” compared to previous recessions.

If we adapt the estimates of lost and postponed consumption by sector in Keogh-Brown et al.1 (which appears to be borne out by high frequency data for Q1 2020) we can get a sense of how big the impacts might be. Even under a “moderate” lockdown, in which only 50 percent of consumers changed their behavior, consumer spending would drop 5 percent in a quarter if the lockdown lasted three weeks. The decline deepens to 9 percent and 18 percent if the lockdown is extended to six and 12 weeks respectively. In a “strict” lockdown where 90 percent of consumers changed their behavior, consumer spending would fall 8 percent in a quarter if lockdown lasted three weeks, worsening to over 30 percent for a 12-week lockdown.

Drastic declines in consumer spending imply steep declines in production and trade too. On the trade front, the evidence of this is already visible. Leading indicators point to a decline in goods trade of over 10 percent year-on-year in March-April, and services trade is likely to fall even faster as sectors such as tourism and air travel have collapsed. As well as weak final demand, trade is likely to be further disrupted by supply chain problems as producers of final goods struggle to source intermediate inputs because of factory closures in other economies. We think total world trade in goods and services could fall by 10-15 percent this year, versus a 10 percent decline during the global financial crisis.

We expect steep declines in output in both advanced and emerging markets (EM). For EM, our baseline forecast is for a decline in GDP of 1.4 percent this year, with the fall in EM excluding China at 3.1 percent. These declines in annual output are smaller than for advanced economies, but that partly reflects the fact that trend growth in EM is somewhat higher than for advanced economies: In December, we forecast EM growth at 4.3 percent for 2020, so the downward revision has been massive. For ex-China EM the scale of the revision is broadly similar to that in advanced economies.

How the Crisis Might Impact Emerging Markets and Advanced Economies Differently

How might the coronavirus crisis impact EM and advanced economies differently? It is risky to generalize about EM too much as there is a great deal of variation across EM. However, there are several possible factors that may lead to EM being more severely — or less severely — affected.

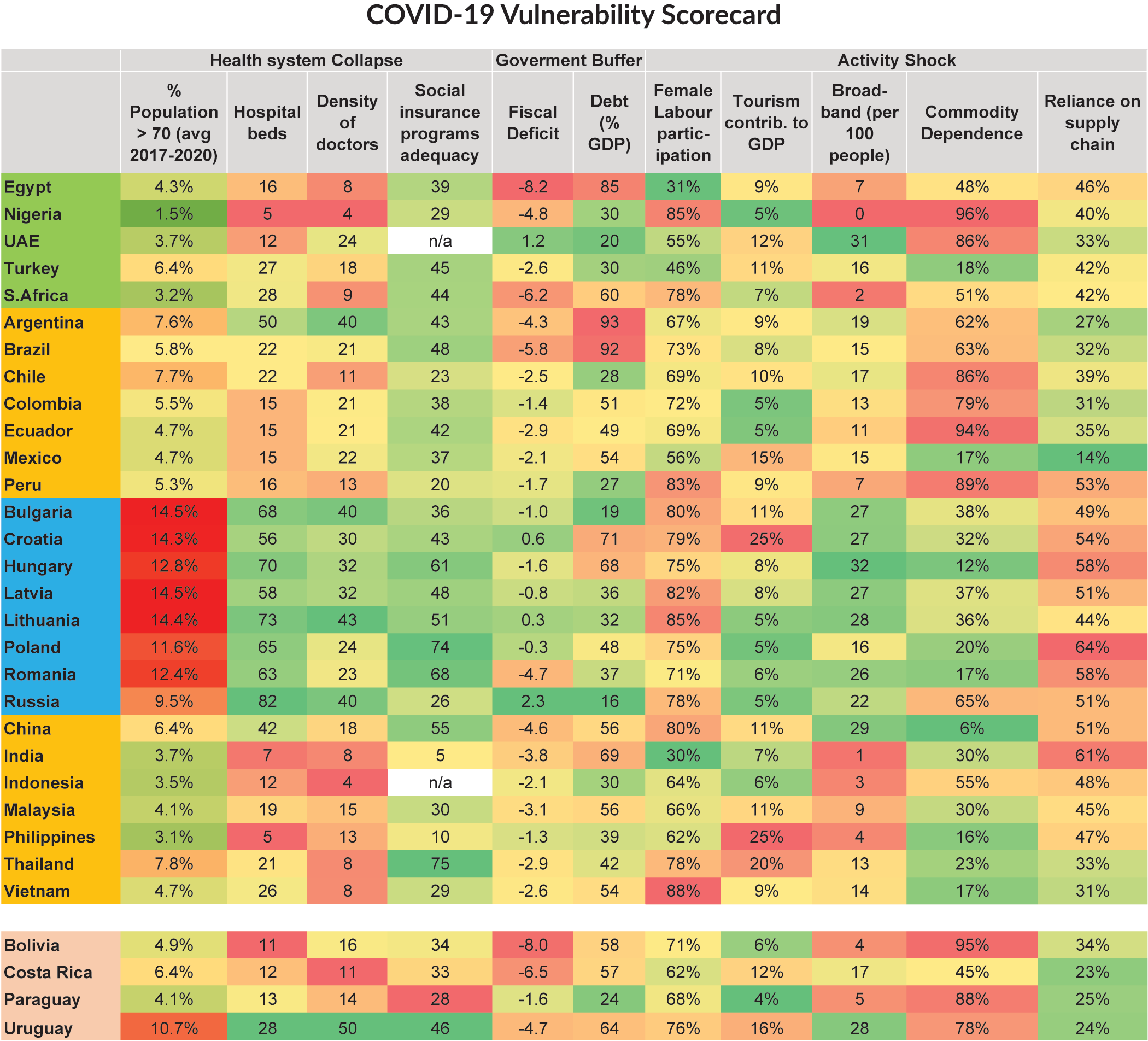

Weak healthcare infrastructure. EM tend to have fewer hospital beds, fewer healthcare professionals, and less specialized medical equipment than advanced economies. This risks healthcare systems being overwhelmed by large numbers of coronavirus cases, so that many people do not get appropriate care and death rates are higher.

Demographics. EM tend to have younger populations than advanced economies. This is an advantage given that elderly people tend to be far more at risk from coronavirus. Demographics and the quality of healthcare systems tend to be negatively correlated: A young population in Nigeria is offset by low levels of health provision while an older population in Hungary goes together with more hospital provision. Looking across EM, the most vulnerable are places like Chile, Peru and Thailand which have both weak health systems and comparatively large numbers of over 70s in the population.

Lack of financial buffers/social security systems. It may be hard to enforce or maintain lockdowns in some EM given weak social security systems and a high share of informal employment (often more than 60 percent) which together mean that such lockdowns will quickly lead to widespread hardship. In many poorer EM, household financial buffers (for example, savings) are also often very limited.

Structural economic vulnerabilities. EM may have structural economic vulnerabilities that make them economically more sensitive to the coronavirus crisis. One of these is reliance on foreign capital inflows to fund budget and/or current account deficits. Since the crisis began, there has been a very strong outflow of foreign capital from EM, worse in scale than in the global financial crisis. This risks leading to rising borrowing costs, liquidity squeezes, and weaker economic growth and government revenues.

Some EM are also heavily reliant on economic sectors that are being especially hard-hit by the crisis such as tourism and commodity production in which huge losses of export earnings are likely. Another potential structural weakness is weak communications infrastructure such as broadband, which may make it hard for workers to work from home/organize online delivery, and so forth. These sectoral vulnerabilities vary across regions but seem highest in Latin America and lowest in emerging Europe.

Another potential structural weakness is high reliance on foreign currency debt, both by governments and the private sector. The slump in capital inflows and related weakening of local EM currencies (by 10-20 percent in some cases since mid-January) threatens to sharply raise the local currency value of their dollar debt.

Lack of fiscal space. Some studies suggest that early and large-scale fiscal interventions are important in curtailing the costs of pandemics. But some EM may lack the fiscal space to do this. In most advanced economies, governments have engaged in massive budgetary actions to try to soften the economic blow of the coronavirus (and of lockdown policies). They have been helped in this by the fact that their bond yields are low and have generally compressed further since the crisis began (partly the result of a “flight to safety”) by investors.

By contrast, many EM look much more constrained on the fiscal side — initial deficits were higher, investors’ tolerance for rising debt and deficits is often lower, and borrowing costs have been rising since the crisis began. Most strikingly, around 20 EM sovereigns’ external debt is trading at “distressed levels” with spreads over U.S. Treasuries of 1,000 basis points or more. These economies owe about $1 trillion of debt or 13 percent of the EM total. Borrowing costs in local currency have also tended to rise, but not in all cases (for example, India and China, where they have fallen). The initial spikes in local currency borrowing costs have also moderated somewhat in several EM recently.

Social conditions. The coronavirus is believed to thrive best in crowded conditions, and thus may spread rapidly in the overcrowded urban areas of some poorer EM. Risks connected with the virus are also linked to poorer general health, again potentially an issue for some EM.

International connectedness/megacities. It appears likely that the coronavirus spread quite early to economies with large cities that are highly internationally connected (for example, New York, London). For many EM, levels of international connectivity are relatively low. This may mean that lockdown policies can be more effective in stopping the progress of the virus quickly — this could also mean lower economic costs.

Looking across different risk factors, the most worrying region looks to be Latin America given its limited fiscal space and structural vulnerabilities. Emerging Europe looks best placed, although painful economic lockdowns may still be needed to protect its relatively high elderly population.

Fiscal Implications of the Coronavirus Outbreak for EM

The massive declines in GDP we expect because of the coronavirus are set to push up budget deficits sharply across the world. Government revenues will slump as economic activity contracts because of lockdowns, social distancing, and the associated slump in output. Meanwhile, government spending will rise on healthcare, social protection including unemployment payments, and explicit policies to tackle the economic impact of the virus such as wage subsidies and support for firms.

These measures are set to push budget deficits in the advanced economies to levels last seen in wartime — we expect deficits in the U.S. and U.K., for example, to reach 20-25 percent of quarterly GDP in Q2 and be 10-15 percent of GDP for the whole of 2020. Recent IMF estimates put the cost of coronavirus-related direct financial support measures globally at $3.3 trillion, loans at $1.8 trillion and guarantees and other contingent liabilities at $2.7 trillion — altogether $7.8 trillion or 5.2 percent of world GDP.

In general, EM direct fiscal packages reported so far are smaller than for advanced economies. Our estimates suggest their median size is around 1.9 percent of GDP versus 2.7 percent of GDP for the advanced economies. Only four governments (Qatar, Thailand, Peru, and Serbia) have announced direct measures in excess of 4 percent of GDP.

Differences are even bigger when we consider “below the line” items such as loans and guarantees. The median size of such packages for advanced economies is around 5 percent of GDP, but for EM zero — over half of EM have done nothing at all in this area.

The smaller fiscal response by EM reflects both negative and positive factors. Negatively, some EM may lack the financial resources, policy credibility, and institutional strength to provide large-scale financial support to the private sector. As a result, their economies could suffer in both the near and longer terms. Notably, some of the biggest packages have come in oil producers such as Kuwait, Qatar, and Saudi Arabia, which have large government assets that they can draw on.

More positively, some EM may have lower requirements for such backstops. The private sector in EM tends to rely less on credit than in advanced economies, reducing the need for loan packages. Lockdowns in EM may also be shorter and less costly given young populations, fewer mortalities, and possibly lower infection rates because of factors like lack of international connectedness mentioned earlier.

Social security systems in EM also tend to be more rudimentary than in advanced economies. As a result, there will be less of a rise in government spending because of “automatic stabilizers,” that is, welfare payments resulting from rising unemployment.

What are the overall consequences for EM budget deficits and debt? Our latest projections for 2020 see the median EM budget deficit being 2.8 percent of GDP worse, than was the case in December last year. This compares favorably with advanced economies in which the median deficit is 4.8 percent of GDP larger. However, EM started from a worse position meaning that their median deficit for 2020 is forecast at 5.7 percent of GDP which is almost the same as for the advanced economies.

Are the forecast rises in EM deficits and debt manageable? It’s important to note that in general tolerance for larger debt and deficits in EM is lower than in advanced economies, and we have already seen that borrowing costs for many EM have risen in recent months — in contrast to advanced economies. Some EM that have relied heavily on foreign purchases of local debt to finance deficits (such as South Africa, Mexico, Indonesia, Colombia, and Poland) also face a challenge in replacing those inflows. That said, it’s notable that many EM have been able to cut interest rates in response to the coronavirus despite looming fiscal deterioration, rather than being forced to put them up as has often happened in crisis periods.

The rises in EM government debt in the medium term that we forecast as a result of coronavirus effects also do not look unmanageable in most cases, with the median debt/GDP ratio for EM remaining below 50 percent of GDP. This is helped by the fact that our forecasts suggest there will be a strong rebound in economic growth from 2021 onwards, which will lead to a rapid improvement in public finances after their deterioration this year. We also note that some EM have actually been able to use quantitative easing — until now the exclusive prerogative of a subset of advanced economies — to help finance deficits and preserve financial stability.

Nevertheless, there may be some EM for which financing pressures are large enough to test market tolerance/cause some financial jitters this year. If we look at both the projected deficit and the value of maturing debt, the total financing needs for Brazil, Hungary, and Ukraine, for example, are over 17 percent of GDP for this year. And even where deficits can be successfully financed via local bond markets this may risk “crowding out” lending to the private sector over the medium term given thin domestic money and capital markets, harming growth.

We can look in more detail at the consequences of fiscal (and other economic) deterioration because of coronavirus for different EM using our Sovereign Risk Indicator, which aggregates data from over 30 variables. Using forecast data for 2020 we can capture the effects of widening budget and current account deficits, increased debt, and higher inflation (resulting from weaker currencies). This exercise shows that overall sovereign risk is set to rise fastest in Oman, Egypt, Croatia, Malaysia, and Thailand.

Overall, the deterioration we are forecasting for EM public finances is very significant in some cases, but less so than in advanced economies. This needs to be weighed against generally lower market tolerance for debt and deficits in EM. Similarly, while a less drastic deterioration in public finances is good news in terms of implying less of a debt build-up for EM compared to advanced economies, it is bad news in terms of less of a backstop being offered to firms and households.

The authorities in EM face something of a balancing act between trying to avoid fiscal efforts being seen as unsustainable (and so spilling over into financial instability) and preventing real economic distress that can spill over into social and political unrest. The danger of the latter seems to be borne out by the correlation over the last decade between GDP disappointments and the prominence of populist movements and/or protests.

FOOTNOTES

1 Marcus Keogh-Brown, Simon Wren-Lewis, W. John Edmunds, Philippe Beutels, and Richard D. Smith, “The Possible Macroeconomic Impact on the UK of an Influenza Pandemic,” University of Oxford Department of Economics Discussion Paper Series No. 431 (May 2009).

END FOOTNOTES